9/6/2012: "Wenn wir beginnen würden, möchten die Probleme lösen, die mit der Finanzpolitik über die komfortabler bedeutet der Geldpolitik .. dann hätten wir ein Problem," sagt Herr Schaeble.

("If we were to begin to want to solve the problems of fiscal policy via the more comfortable means of monetary policy ... then we would have a problem," said Mr. Schaeuble)

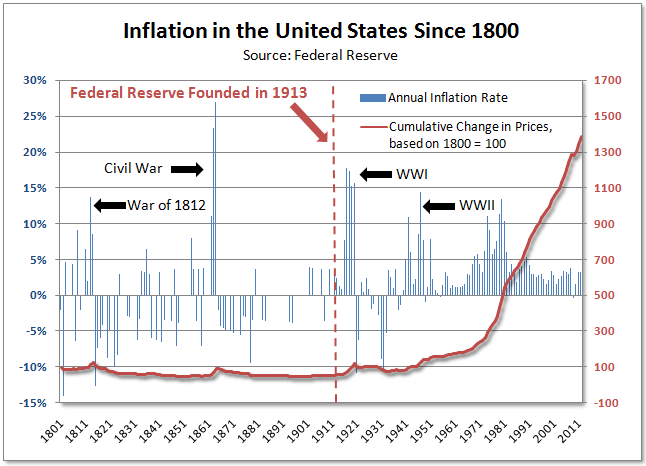

The Fed fails to grasp that an interest rate is a price, the price of time. Attempting to manipulate that price is as destructive as any other government price control

To know what is wrong with the Federal Reserve, one must first understand the nature of money. Money is like any other good in our economy that emerges from the market to satisfy the needs and wants of consumers. Its particular usefulness is that it helps facilitate indirect exchange, making it easier for us to buy and sell goods because there is a common way of measuring their value. Money is not a government phenomenon, and it need not and should not be managed by government. When central banks like the Fed manage money they are engaging in price fixing, which leads not to prosperity but to disaster.

The Federal Reserve has caused every single boom and bust that has occurred in this country since the bank's creation in 1913. It pumps new money into the financial system to lower interest rates and spur the economy. Adding new money increases the supply of money, making the price of money over time—the interest rate—lower than the market would make it. These lower interest rates affect the allocation of resources, causing capital to be malinvested throughout the economy. So certain projects and ventures that appear profitable when funded at artificially low interest rates are not in fact the best use of those resources.

Eventually, the economic boom created by the Fed's actions is found to be unsustainable, and the bust ensues as this malinvested capital manifests itself in a surplus of capital goods, inventory overhangs, etc. Until these misdirected resources are put to a more productive use—the uses the free market actually desires—the economy stagnates.

The great contribution of the Austrian school of economics to economic theory was in its description of this business cycle: the process of booms and busts, and their origins in monetary intervention by the government in cooperation with the banking system. Yet policy makers at the Federal Reserve still fail to understand the causes of our most recent financial crisis. So they find themselves unable to come up with an adequate solution.

In many respects the governors of the Federal Reserve System and the members of the Federal Open Market Committee are like all other high-ranking powerful officials. Because they make decisions that profoundly affect the workings of the economy and because they have hundreds of bright economists working for them doing research and collecting data, they buy into the pretense of knowledge—the illusion that because they have all these resources at their fingertips they therefore have the ability to guide the economy as they see fit.

Nothing could be further from the truth. No attitude could be more destructive. What the Austrian economists Ludwig von Mises and Friedrich von Hayek victoriously asserted in the socialist calculation debate of the 1920s and 1930s—the notion that the marketplace, where people freely decide what they need and want to pay for, is the only effective way to allocate resources—may be obvious to many ordinary Americans. But it has not influenced government leaders today, who do not seem to see the importance of prices to the functioning of a market economy.

The manner of thinking of the Federal Reserve now is no different than that of the former Soviet Union, which employed hundreds of thousands of people to perform research and provide calculations in an attempt to mimic the price system of the West's (relatively) free markets. Despite the obvious lesson to be drawn from the Soviet collapse, the U.S. still has not fully absorbed it.

If there is one thing Barack Obama has proven throughout the first term of his presidency besides his expert use of grandiose, simplistic rhetoric, it is his ineptness at understanding economics. Last year, the President hilariously blamed automatic teller machines and kiosks for unemployment. Because politics is defined by reactionary and short term consideration, Obama doesn’t see the additional employment and capital surpluses that result by eliminating labor costs.

Such Luddite-esque thinking often provides all the more justification for government interference [the cause of US economic failure] in the marketplace to try and equalize outcomes. This view is paired with the perception that rather than society giving legitimacy to the state first, the state and its enforcers are destined to guide society. Under the pretenses of promoting the public good, [Soviet-like] central planners see failure not as a necessary process of the market but an opportunity to usurp more authority. Ludwig von Mises accurately recognized the inevitable goal of economic regulation decades ago:

Interventionism cannot be considered as an economic system destined to stay. It is a method for the transformation of capitalism into socialism by a series of successive steps.

Nowhere is this more prevalent than in today’s financial sector. The recent $2 billion trading loss by Wall Street giant JP Morgan has given more ammo to the crowd that wishes Washington to have more of a say over the operation of the big banks. Obama, ever the politician, has taken the loss as an opportunity to tout the merits of banking regulation. In an interview on the daytime talk show The View, the popular ladies get his thoughts on Jamie Dimon’s big flub. From McClatchy:

WHOOPI GOLDBERG: So now I’m wondering because I watched this JP Morgan Chase thing just go down. I’m wondering (A) what do you think happened and (B) sir what are you going to do about it because this has to be the last straw.

PRESIDENT BARACK OBAMA: Well look, first of all, JP Morgan is one of the best managed banks there is. Jamie Dimon the head of it is one of the smartest bankers we got and they still lost $2 billion dollars and counting precisely because they were making bets in these derivative markets. We don’t know all the details yet. It’s going to be investigated, but this is why we passed Wall Street reform. The whole point was, even if you’re smart, you can make mistakes and since these banks are insured backed up by taxpayers, we don’t want you taking risks where eventually we might end up having to bail you out again, because we’ve done that, been there, didn’t like it.

BARBARA WALTERS: Specifically, though, Mr. President, you have all of these things in place, some working, some not. Are you — is the federal government going to do anything more so that this doesn’t happen?

The Fed fails to grasp that an interest rate is a price—the price of time—and that attempting to manipulate that price is as destructive as any other government price control. It fails to see that the price of housing was artificially inflated through the Fed's monetary pumping during the early 2000s, and that the only way to restore soundness to the housing sector is to allow prices to return to sustainable market levels. Instead, the Fed's actions have had one aim—to keep prices elevated at bubble levels—thus ensuring that bad debt remains on the books and failing firms remain in business, albatrosses around the market's neck.

The Fed's quantitative easing programs increased the national debt by trillions of dollars. The debt is now so large that if the central bank begins to move away from its zero interest-rate policy, the rise in interest rates will result in the U.S. government having to pay hundreds of billions of dollars in additional interest on the national debt each year. Thus there is significant political pressure being placed on the Fed to keep interest rates low. The Fed has painted itself so far into a corner now that even if it wanted to raise interest rates, as a practical matter it might not be able to do so. But it will do something, we know, because the pressure to "just do something" often outweighs all other considerations.

What exactly the Fed will do is anyone's guess, and it is no surprise that markets continue to founder as anticipation mounts. If the Fed would stop intervening and distorting the market, and would allow the functioning of a truly free market that deals with profit and loss, our economy could recover. The continued existence of an organization that can create trillions of dollars out of thin air to purchase financial assets and prop up a fundamentally insolvent banking system is a black mark on an economy that professes to be free.

U.S. Treasury Secretary Jack Lew proudly announced that for the fiscal year ended Sept. 30, 2014, the federal government collected the most tax revenue ever: $3.013 trillion. But despite record taxes, the federal government spent $483 billion more than it took in.

To paraphrase Ronald Reagan, we don't have a $17.8 trillion debt because we have not taxed enough. We have a $17.8 trillion debt because we spend too much.

Obviously, the federal government's strategy of taxing our way to a balanced budget is not working. The more money that is collected, even more money is spent. Taxes aside, the budget has little chance of ever being balanced (or producing surpluses) unless the government stops spending as much.

There have been recent efforts at spending cuts. There were across the board cuts in discretionary government programs (sequestration) and capping future discretionary spending. Both helped. But they were more than offset by mandatory increases in entitlement programs, expanding populations in the entitlement programs and new programs like Obamacare.

That is because entitlements are the main driver of increased spending. Medicare, Medicaid, Social Security and other entitlements currently account for 55 percent of the federal budget. Without entitlement reform, their mandatory rate of growth will overwhelm the rest of the budget. That means crowding out the defense budget (20 percent) and all other government spending (17 percent).

And when the federal government does not have all the money to pay its bills, it borrows. Interest payments on the federal debt represent 7 percent of the federal budget. By the way, the average interest rate paid on the $17.8 trillion of debt is 2.3 percent. Imagine how much interest would be paid when interest rates normalize, say at 5 percent.

The problem is that cutting spending is hard work and requires unpleasant choices. So instead of tackling them now, the president and Congress are content to kick the can down the road. But soon that road will run out and there will be fewer choices and less time for a solution.

Big spending requires big revenues to pay for that spending. All those tax revenues take hard-earned money away from Americans, who would use their money on what they think is important. And whether they spend it, save it or invest it, the end result is a big boost to the economy.

But when the federal government gets that money, it spends it on what it thinks is important. Because of the political process and bureaucracy, it is inherently an awful and inefficient allocator of resources. Think of it this way: Are Americans better off if a family cannot buy a refrigerator so that mountain lions can be trained to walk on treadmills?

I would rather rely on the people making choices. Cut spending and taxes, and have the people decide on how best to use their money. They and our country will be better off.

“The more power the government has, the greater the risk to the people and the more dangerous the abuse.” Edmund Burke, 1771.

Big government is organized crime in all but name, and the man in the street is numb to the universal risk in today’s world.

Politicians and bureaucrats are spending the world into oblivion while secretly hoping and expecting to escape debt with depreciated dollars: yours. The public is unaware.

Note that your “elected” politicians never talk about the ongoing depreciation (inflation) of paper money (U.S. dollars). They don’t want you to think about this. They would rather you think about Donald Sterling and his frivolous racial comments.

But you should be on high alert. Liquidity is not only negative; it is at its most negative level in history. Are we facing the second Great Depression or worse?

For the third time in 14 years, U.S. stocks are in a bubble and far more leveraged than ever before. There are now more corporate bonds outstanding in the U.S. than there are mortgage-backed securities. This is significant, and the heart of the next crisis and the debt bubble will be non-financial corporate debt.

Investors beware! Stockholders beware!

Thanks to the Fed, it now seems that we have a bubble in all asset classes much larger than 2007. The Fed and other central banks with their expansionary monetary policies, all designed to boost asset prices, are similar to a juggler who is trying to keep all his balls in the air. The Big One is coming and there will be no place to hide except in very depressed gold stocks.

John Adams said, “Without [term limits] every man in power becomes a ravenous beast of prey”. That being said, here are some of the reasons we believe our country needs Term Limits.

Term Limits can help break the cycle of corruption in Congress. Case studies show that the longer an individual stays in office, the more likely they are to stop serving the public and begin serving their own interests.

Term Limits will encourage regular citizens to run for office. Presently, there is a 94% re-election rate in the House and 83% in the Senate. Because of name recognition, and usually the advantage of money, it can be easy to stay in office. Without legitimate competition, what is the incentive for a member of Congress to serve the public? Furthermore, it is almost a lost cause for the average citizen to try to campaign against current members of Congress.

Term Limits will break the power special interest groups have in Congress.

Term Limits will force politicians to think about the impact of their legislation because they will be returning to their communities shortly to live under the laws they enacted.

Term Limits will bring diversity of people and fresh ideas to Congress.

[Editor's Note: If you want to get rich, i.e. advance from a low paying government bureaucrat job on the local or state level, THEN GET ELECTED TO THE US CONGRESS (House or Senate). Once you're elected, it's easy to steal from your campaign contributions or the Congressional budget allocated to your seat and staff. You can go on a government-funded junket with 'lavishly' paid expenses. The list of ways to steal from the government while in office is inexhaustible. There are only a few Congressmen who left Congress just wealthy instead of a multi-millionaire. Of course, there are several who arrived in Congress as multi-millionaires and don't need to steal from the government.]

[Editor's Note: what I have dubbed the "Legislative-Executive-Judicial Cabal" which the American People have caused by ignoring the generational transition from our Constitutional Republic to what now is, in effect, an "elected" dictatorship. Never mind who is elected. Never mind which bogus party is in power. We the People still lose more freedom.

A Constitutional Convention is necessary to amend the Constitution for Congressional Term Limits to twelve (12) years and restrict time in DC to only six (6) months per year. Such an Amendment is only a FIRST step in restoring America to its Constitutional roots. Back in the day when the People still feared kings, the president's term was limited by Constitutional Amendment.

Currently, CONgress is just a group of socialists, progressives, and faux-conservatives (career politicians) that, on a daily basis, ignores the Constitution, many of their own past statutes, and cedes their responsibilities to the president ("elected" dictator). A comparison to the history of Rome becomes more and more credible with the Executive and its "featherbedded" lackeys gaining more power while CONgress sits back all fat-dumb-and-happy.

CONgress has made recent efforts to expose State Dept. failures in Benghazi (inept political leader), Fast-and-Furious gun-running (criminal AG), IRS 1st amendment violations, gov't union Veterans Administration fraud, and whining about Obama(Reid)-killer-Care, but these efforts are mostly politics as usual. Most "citizens" will forget about these infringements from our unaccountable, uncontrollable Executive branch with its tyrannical agencies staffed by socialist unions that extort "juicy" contracts from the "elected" dictatorship.

Most positions in the federal government whether elected, appointed, or hired are nominal, make-work jobs (confidentially) designed merely to grow government, bilk money from private businesses and citizens, and eventually fully transform America into a totalitarian state. When this happens, CONgress will have destroyed the economy and the country by their negligence and counter-liberty policies, and it will be almost impossible to Restore America. The 'Restore America' list is only a beginning too.]

The FairTax is a consumption tax unilaterally applied to all Americans at the same rate. For businesses, payroll taxes would no longer exist. Our exports would include a heavy tax for overseas buyers purchasing our products, while our imports would be cheaper for us to purchase. I'm not sure how this would affect GDP, as more information is necessary.

According to the FairTax website, "Under the FairTax, every person living in the United States pays a sales tax on purchases of new goods and services, excluding necessities due to the prebate." The prebate gives every legal resident household an "advance refund" at the beginning of each month so that purchases made up to the poverty level are tax-free.

So a family of four making something like $50,000/year should not have to pay taxes, thus preventing an unfair burden on low-income families. Since the FairTax eliminates both federal and payroll taxes, you get to keep your gross pay amount of each paycheck earned.